In financial services, many firms are focused on providing bottom-line value to their clients. What most of them forget is how to properly communicate that value.

A good PR strategy has a greater impact on the bottom line than most firms realise. This book shows how to put in place an effective PR program in the financial services industry, and how great communications can add significant value to a firm.

Between them, Claudia Pritchitt and Leeanne Bland have over 50 years’ experience in public relations, communications, and marketing. Here, they explain the key tools needed in an effective communications strategy as well as why plain English is imperative in the jargon-heavy world of financial services.

Throughout the first half of 2025, we have been more optimistic than the consensus on the ability of equities to absorb and/or look through downside risks. On April 9th, when US President Trump paused the implementation of tariffs, we took the view that this signalled a peak in trade and growth-related uncertainty and pivoted back towards risk assets. Since then, we’ve ridden the wave higher without the accompanying fear of doing something wrong.

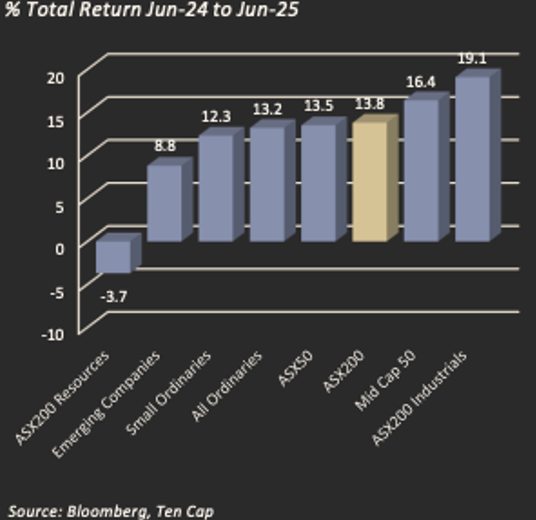

A solid year for Australian equities

It’s hard to calibrate the size of the rally (large) versus the improvement in fundamentals (limited). But if a US recession and loss of US exceptionalism are the downside markers for expectations, then it does not take a lot to be positively surprised, and modest “risk-on” positioning, better than expected news flow on both the macroeconomic and corporate profit backdrop have been powerful tailwinds for the equity rally since the April lows.

With most major equity markets at all-time highs and volatility measures (VIX) back to where they stood at the start of the year, it is possible that there are some elements of complacency creeping in, particularly as the growth outlook has weakened and remains highly uncertain. But we think equity markets are showing a high degree of resiliency via their repeated ability to absorb downside risks and we think this is a solid base for further gains as we move into the second half of the year.

There are a lot of downside risks to consider. Tariff negotiations are still ongoing, geopolitical risks remain elevated, the Middle East remains on high alert following the recent Israel-Iran conflict, commodity prices have been extremely volatile, central banks are easing but with a hawkish tone, the risk premium for equities is paper thin and there is widespread distrust in the equity rally from April lows.

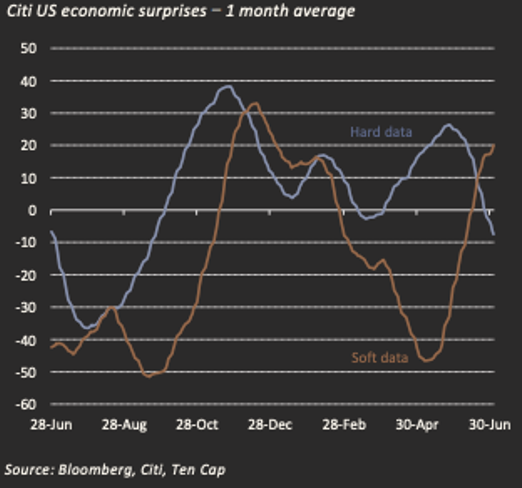

US “soft” and “hard” data convergence

But when investing in risky assets, there are always risks to navigate regardless of where markets are trading. For instance, when valuations are low, we worry that earnings fundamentals won’t catch up and grow into valuations. And, when valuations are high, we worry that fundamentals are about to weaken and cannot support optimism built into share prices.

The question is whether the current set of risks are enough to dislodge the trajectory of equity markets if positive drivers are also gaining momentum. We don’t think this will be the case and expect equities to continue climbing a wall of worry through 2H25 – maybe not in a straight line – but certainly with an upward bias.

ASX200 hits a record high

At this stage, and outside of a US recession, we think there are enough positive tailwinds to offset short term headwinds and that equity fundamentals - namely improving earnings and easier policy settings - will continue support the market as we move deeper into 2H25. We believe these tailwinds will be a sufficient bridge to traverse a short period where markets look like they are trading ahead of fundamentals for five key reasons:

The equity market is approaching and pricing in policy and/or geopolitical risks through an isolation lens. The initial reaction is negative, but the market is quickly filtering and then calibrating these risks with price stability emerging relatively quickly. We have seen this with concerns around US fiscal spending which drove a short spike in bond yields and then more recently with the escalation in Middle East tensions between Israel and Iran.

The Fed, while not outwardly dovish, has been softening its stance towards further policy easing as the threat of a near term (tariff driven) inflation spike has decreased. In fact, survey data shows that expected price increases are yet to show through in hard data. In part this can be explained by corporates holding off on pushing through price increases and running down inventory. We think the threat of a sharp trade driven US inflation spike is relatively contained and this bodes well for further policy rate support by the Fed

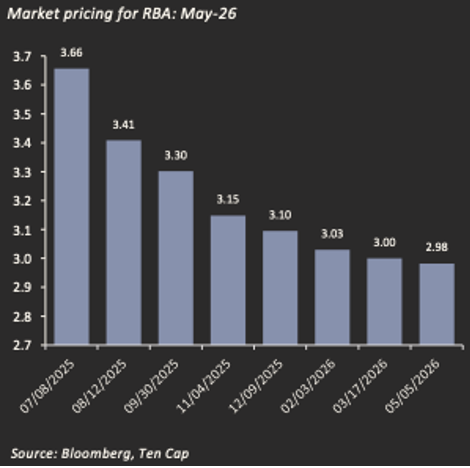

Australia’s May CPI print, which was better than expected at both a headline and core level and showed a favourable mix with services and housing both stepping down, has provided a strong green light for the RBA to cut faster and deeper. If neutral is around 3.00% and rates are currently at 3.85%, then we think households should expect at least another 100bps of easing but likely more if rates need to fall back into an easy setting.

As Gerard Minack (Minack Advisors) points out, in real terms the cash rate was zero or negative for 6-7 years before the pandemic and there was no evidence that this was stimulative. If the neutral rate remains zero or less in real terms – and he doesn’t see any reason why it should have risen – then the RBA can cut the nominal rate to 2½% or less – another 125-150bps! That might not fix Australia’s structural growth problems, but it will certainly fire up the domestic equity market and house prices.

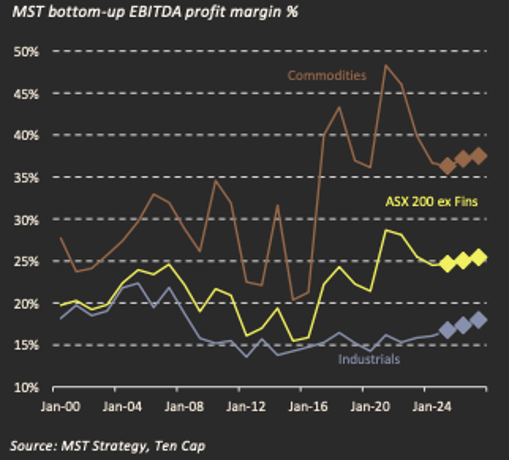

ASX200 profit margins expected to rise

We think we are past the worst for both earnings' revision momentum and earnings growth. While it might take some time for a broader cyclical improvement to be seen in corporate earnings, elevated profit margins should support solid operational leverage in the early stages, particularly with corporates not likely to require additional labour. We think ~10% eps growth for the industrial universe is achievable off the back of modest margin gains which should again see a strong divergence in equity gains for cyclical vs non-cyclical stocks. In addition, outside of a recession, we think the resource sector is not far off cyclical earnings lows and this offers upside potential for the broader earnings backdrop against tepid growth for the banks.

We think positioning and sentiment supports further gains for the equity market. Institutional investors were quick to cut equity risk as we moved into late 1Q25 / early 2Q25 off the back of rising US growth concerns. In addition, there was a large amount of de-risking that was undertaken by hedge funds as a whipsawing market saw performance drop sharply.

As a result, when the market turned up in early April, institutional clients were late to the rally and have been chasing it higher ever since. Sentiment and positioning data does not show that equity investors are either excessively bullish or overweight equity allocations. If macroeconomic conditions continue to normalize, we think positioning will remain a positive tailwind.

Finally, a lot has been made of the performance of Commonwealth Bank (ASX.CBA) through FY2025 where it rose ~45% to become the largest stock in the market. We have written extensively on this (see CBA has become the “Magnificent One” – June-25) but don’t see the performance of Commonwealth Bank as important for the overall market outlook in FY26. because its not a precursor to another solid year for Australian equities despite its size.

In fact, we would argue that a more moderate return year for Commonwealth Bank is beneficial for the market outlook as it does not suck capital out of other areas (in particularly the mid and small cap index plays) and it does not provide such a large distortion for aggregate returns.

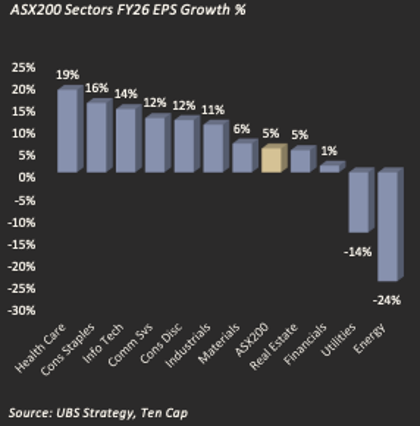

Australian EPS growth looking strong

But more importantly, the return for Commonwealth Bank is not a marker for how other stocks perform as evidenced by the significant returns skew seen from sectors such as consumer retail, telecom services, industrials and technology stocks through FY25. A more balanced and less dispersed stock return profile should signal a more robust and resilient equity market which is good for everyone!

Putting this all together, we think the tailwinds from offshore will remain relatively favourable (at least not deteriorating to any meaningful degree) while at the same time domestic drivers will gradually strengthen as the RBA eases policy settings. Historically a policy rate-cutting cycle outside of an economic recession is very bullish equity markets.

It is not often that Australia is a relative safe haven when the US is softening. But the US is kicking own goals and outside of a recession, we think Australia can avoid the worst of these drags. While valuations are elevated, we have repeatedly argued that they are not a constraint to the domestic equity market trading higher, particularly when cyclical tailwinds are building.

Summary

If we are at the start of a cyclical upswing, even if moderate in amplitude versus history, then equities will remain a decent place to be. No doubt investors will need to hold onto their conviction given an uncertain and volatile backdrop. But we think they will be rewarded with another solid year from large cap stocks and an even better year as we move down the market cap spectrum into mid and small caps. We have argued that investors should stare into risks rather than run from them and we maintain this view.

RBA rate expectations have collapsed

We think the Australian equity market will grind its way higher through year end and has the potential to finish with mid “teen” returns. This will be driven by a combination of earnings upside as well as multiple expansion – particularly in the commodity and laggard cyclical related areas.

For some time there has been a strong style tilt towards growth stocks and away from value stocks. At first this was driven by the hunt for earnings growth, but this gradually transformed into defensive (structural) growth and away from cyclical weakness. The valuation dispersion (expensive growth / cheap value) makes the style call less obvious, but we push back against the consensus call that value will meaningfully outperform. We think investors will be more focused on relative value and this is more agnostic to a style preference.

Ultimately, we think investors will be surprised by how resilient equity markets are to ongoing risks and volatility. The desire to reposition and add to equity allocations appears strong with Australia remains well insulted from global trade concerns. In addition, the RBA is in the fortunate spot of facing less severe trade driven inflation fears which should open it up to a more aggressive easing path. At present, market expectations are for an additional 75bps of easing by year end (down to 3.10%). We think this is a minimum rather than a maximum level of easing likely to take place before the cash rate bottoms for the cycle. These are market friendly conditions even if there are a few thorns in the side of the call.