In financial services, many firms are focused on providing bottom-line value to their clients. What most of them forget is how to properly communicate that value.

A good PR strategy has a greater impact on the bottom line than most firms realise. This book shows how to put in place an effective PR program in the financial services industry, and how great communications can add significant value to a firm.

Between them, Claudia Pritchitt and Leeanne Bland have over 50 years’ experience in public relations, communications, and marketing. Here, they explain the key tools needed in an effective communications strategy as well as why plain English is imperative in the jargon-heavy world of financial services.

Super funds posted another strong result for the 2025 calendar year, with the median growth fund (61–80 per cent in growth assets) returning 9.3 per cent. This follows impressive gains of 9.9 per cent in 2023 and 11.4 per cent in 2024, translating to nearly 35 per cent growth over the past three years. Super fund members invested in higher-risk portfolios enjoyed even stronger outcomes.

Chant West senior investment research manager, Mano Mohankumar, says international share markets were the key driver of 2025’s strong performance, delivering 18.6 per cent on a currency-hedged basis, despite uncertainty around tariffs and geopolitical tensions.

“International shares in unhedged terms was lower, with a 12.5 per cent return due to the appreciation of the Australian dollar over the year (up from US$0.62 to US$0.67). On average, growth funds have 31 per cent in total invested in international shares and 25 per cent allocated to Australian shares, with Australian shares also contributing meaningfully, returning 10.7 per cent. It also helped that all major asset classes generated positive returns over the period.

“We’re still in the process of collecting final returns for unlisted asset classes such as unlisted property, unlisted infrastructure and private equity, all of which were in positive territory. We estimate that unlisted infrastructure finished with gains in the 7 per cent to 10 per cent range, with private equity likely to finish with a low double-digit return. Unlisted property, which was in the red in each of the two previous years, is expected to finish with a positive return in the 3 per cent to 6 per cent range. Listed real assets were also up, with Australian listed property returning 9.7 per cent, while international listed property and international listed infrastructure yielded gains of 7.5 per cent and 11.6 per cent, respectively. Within the traditional defensive asset classes, cash, Australian bonds and international bonds returned 4 per cent, 3.2 per cent and 4.4 per cent, respectively.

“With share markets performing so well in 2025, particularly international shares, naturally the better performing super funds generally had higher allocations to those asset classes. Funds that had lower allocations to unlisted property, cash and bonds would have also benefitted, as did those with lower exposure to the US dollar,” said Mohankumar.

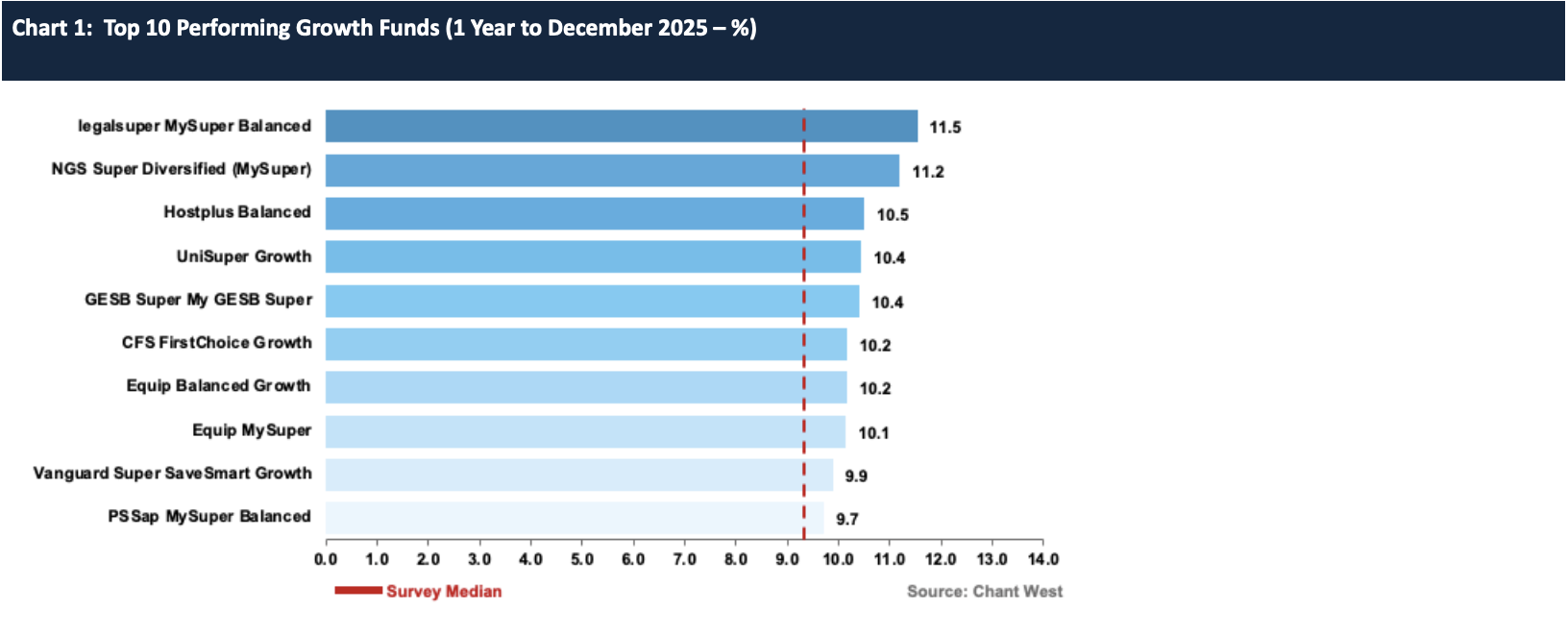

Chart 1 shows the top 10 performing growth options over the 2025 calendar year, together with the survey median, noting that long-term performance is more important for super fund members.

Notes:

1. For inclusion in the Top 10, investment options must have been in the Growth category for the full year and where an investment option is not a fund’s main option in the Growth category, it must also meet a minimum size requirement of $1 billion.

2. Performance is shown net of investment fees and tax. It is before administration fees.

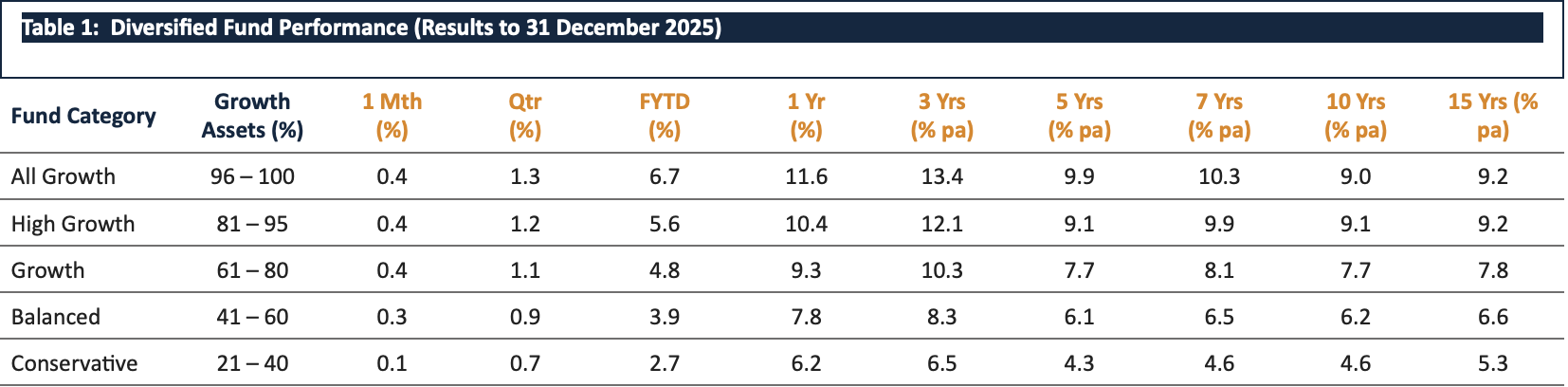

Table 1 compares the median performance for each of the traditional diversified risk categories in Chant West’s Super Fund Performance Survey, ranging from All Growth to Conservative. Over the long term, all risk categories have met their typical return objectives, which range from CPI + 1.5% for Conservative funds to CPI + 4.25% for All Growth.

Note: Performance is shown net of investment fees and tax. It is before administration fees and adviser commissions.

Source: Chant West

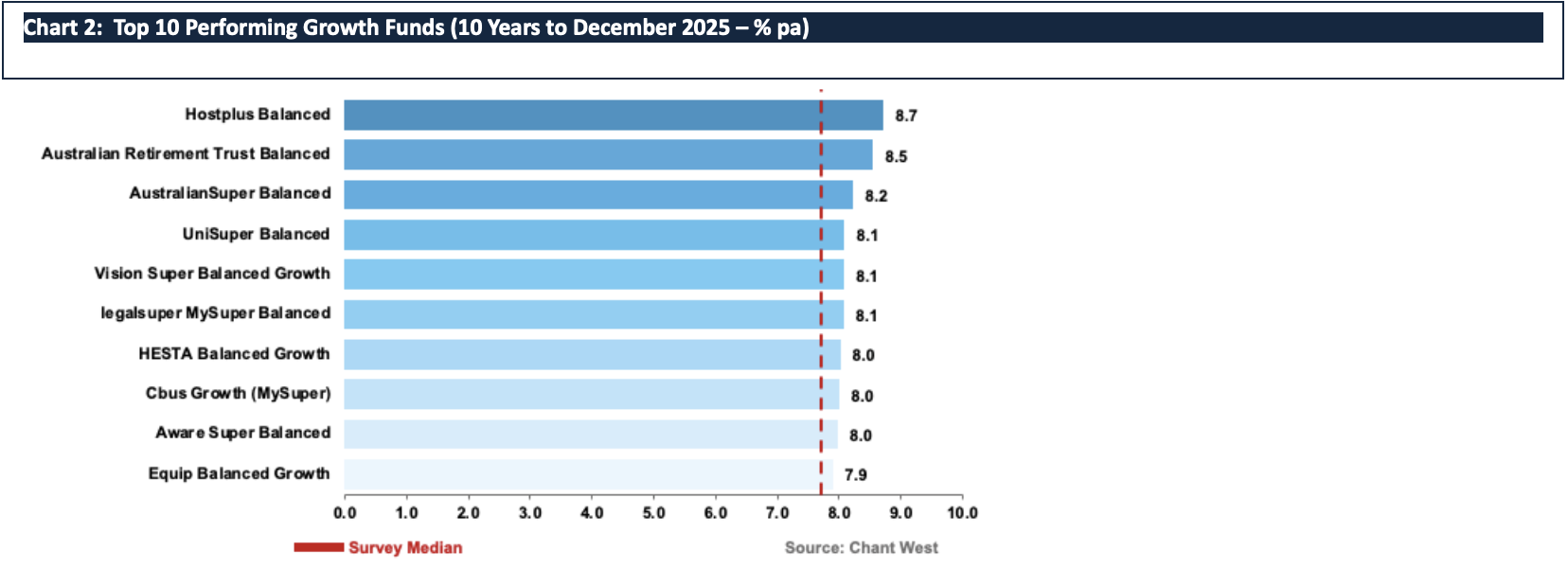

Chart 2 shows the top 10 performing growth options over 10 years, together with the survey median.

Notes:

1. For inclusion in the Top 10, investment options must have been in the Growth category for the full 10 years and where an investment option is not a fund’s main option in the Growth category, it must also meet a minimum size requirement of $1 billion.

2. Performance is shown net of investment fees and tax. It is before administration fees.

Funds continue to beat risk and return targets

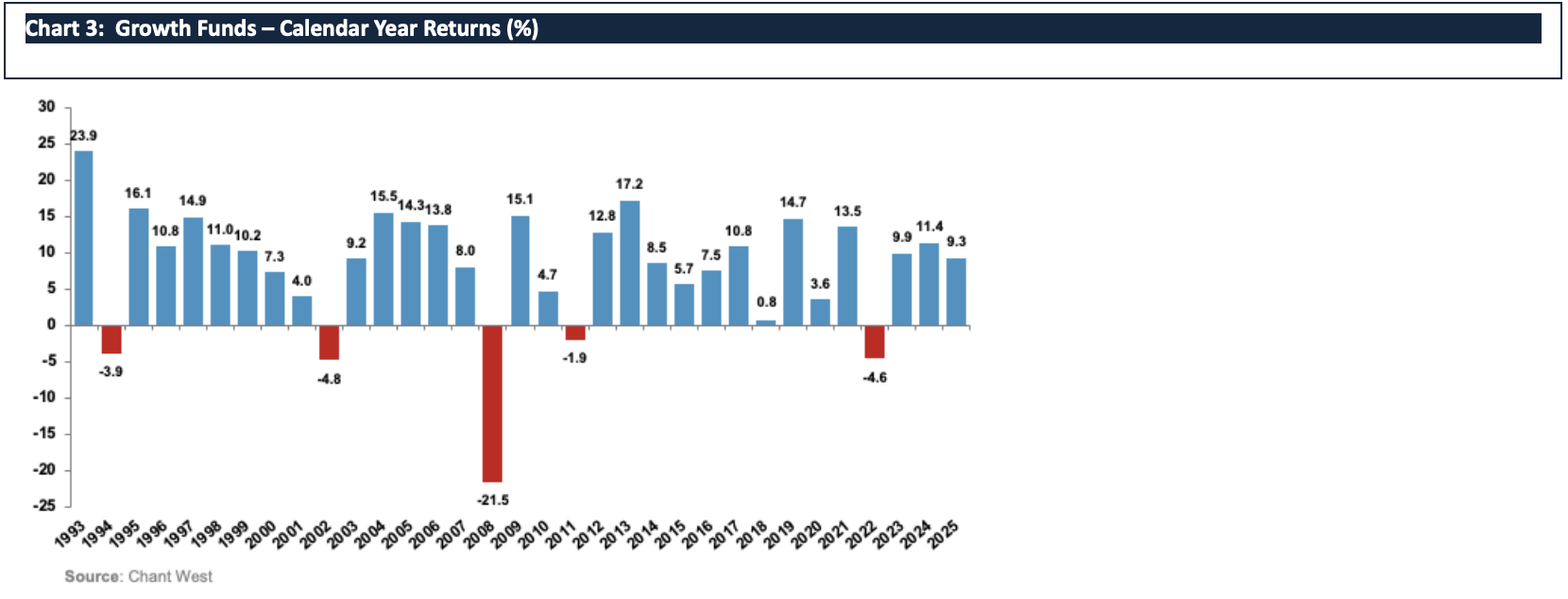

While much of the focus at this time of year is on calendar year performance, Mohankumar believes fund members always need to think long term. To provide further context, Chart 3 plots the year-by-year performance of the median growth fund over the full 33 calendar years since the introduction of compulsory super in July 1992. It shows that super funds have delivered on their risk and return objectives over the long term.

Mohankumar says that while super funds had a strong 2025 with a median return of 9.3 per cent, that level of return shouldn’t be thought of as normal.

“The typical long-term return objective for growth funds is to beat inflation by 3.5 per cent a year, which translates to just over 6 per cent a year. Since the introduction of compulsory super, the annualised return is 8 per cent and the annual CPI increase is 2.7 per cent, giving a real return of 5.3 per cent a year – well above that 3.5 per cent target. Even looking at the past 20 years, which includes three major share market downturns – the GFC in 2007-2009, COVID-19 in 2020 and the high inflation and rising interest rates in 2022 – super funds have returned 6.9 per cent a year, which is still comfortably ahead of the typical objective.

“Returns are important but so is risk, and most funds also set themselves a risk objective. Risk is normally expressed as the likelihood of a negative annual return, and typically a growth fund would aim to post no more than one negative return in five years on average. This objective would translate to no more than six negative years over the 33 calendar years shown. As it turns out, there have only been five, so the risk objective has been met as well as the performance objective.”

Note: Performance is shown net of investment fees and tax. It does not include administration fees.

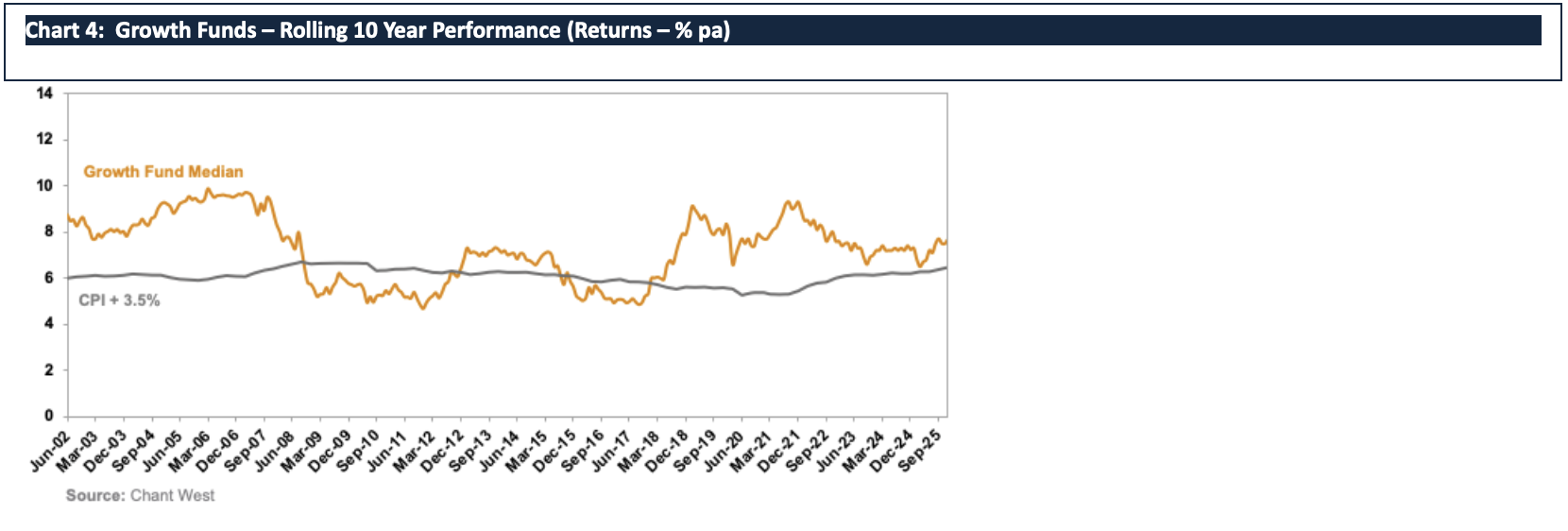

Long-term performance remains above target

Chart 4 shows that for most of the time since compulsory super, the median growth fund has exceeded its return objective over rolling 10-year periods, which is a commonly used timeframe consistent with the long-term focus of super. The exceptions are two periods between mid-2008 and late-2017, when it fell behind. This is because of the devastating impact of the 16-month GFC period (end-October 2007 to end-February 2009) during which growth funds lost about 26% on average.

Note: The CPI figure for the December 2025 quarter is an estimate.